TL;DR:

- Understanding what constitutes a qualified energy project is essential for accessing significant tax credits, incentives, and financing. Different federal, state, and IRS definitions impact eligibility, aggregation rules, and project valuation, which can greatly influence financial outcomes. Investors who grasp these nuances and structure deals accordingly can maximize returns and secure competitive advantages in the energy sector.

If you’re evaluating energy sector investments, understanding what is a qualified energy project is not optional. It determines whether you can access six-figure tax credits, state-level property tax exemptions, and federally backed financing. Yet most investors treat “qualified energy project” as a single, uniform category when it’s actually a cluster of distinct legal definitions spread across federal statutes, IRS regulations, and state programs. Getting the distinction wrong costs real money.

Table of Contents

- Key takeaways

- What qualifies an energy project: definitions and eligibility criteria

- Tax benefits from qualified energy projects

- IRS aggregation rules and project qualification nuances

- State programs and real-world examples

- My perspective: what most investors miss about qualified energy project eligibility

- How Fieldvest helps you invest in qualified energy projects

- FAQ

Key takeaways

| Point | Details |

|---|---|

| No single definition exists | “Qualified energy project” means different things under federal tax law, state programs, and IRS regulations. |

| Technology type drives eligibility | Solar, wind, advanced energy manufacturing, and storage all qualify under different credit programs with distinct rules. |

| IRS aggregation rules matter | Multiple facilities may be treated as one project, affecting how credits and adders are calculated. |

| State programs add significant value | Ohio and Texas offer property tax abatements and low-interest loans that stack on top of federal incentives. |

| The 80/20 rule opens retrofit plays | Retrofitted facilities with up to 20% used components can still qualify as newly placed in service. |

What qualifies an energy project: definitions and eligibility criteria

The phrase “qualified energy project” appears in multiple legal contexts, each with its own eligibility rules. No single federal statute governs all of them. Investors need to identify which program they’re analyzing before assessing eligibility.

Under the IRS framework, a qualified energy project is broadly any facility that generates electricity or heat using qualifying technologies and meets the technical and financial thresholds specified for a given credit. The most referenced federal credits are the Section 48 Investment Tax Credit (ITC), the Section 48E technology-neutral ITC, and the Section 48C Qualifying Advanced Energy Project Credit.

The core eligibility criteria investors should know are:

- Technology type: Solar photovoltaic, wind, geothermal, hydropower, fuel cells, combined heat and power (CHP), energy storage, and offshore wind all qualify under Section 48. Section 48E extends to any zero-emission electricity technology, not just the listed types.

- Capacity thresholds: Some programs require minimum generating capacity; others impose maximums for automatic approval. Ohio’s program, for instance, triggers county board review for projects exceeding 20 MW.

- Greenhouse gas benchmarks: The 48C credit requires qualifying industrial retrofits to reduce greenhouse gas emissions by at least 20%, with $10 billion in total allocated funding.

- Placed-in-service date: When a project is officially commissioned affects which credit regime applies. Projects placed in service before 2025 fall under legacy Section 48; those after fall under Section 48E.

- Labor standards: Prevailing wage and registered apprenticeship requirements now apply to maximize credit percentages under the Inflation Reduction Act (IRA).

Pro Tip: Before modeling any energy investment, identify which specific credit program governs the project. Running Section 48 numbers on a project that actually qualifies under 48E, or vice versa, will produce the wrong tax picture.

One area investors frequently miss is the difference between manufacturing-side and generation-side projects. A solar panel factory that reduces its carbon footprint can qualify under 48C as an advanced energy project. The solar farm it supplies qualifies separately under Section 48. Both are “qualified energy projects,” but they operate under entirely different eligibility criteria.

Tax benefits from qualified energy projects

Federal tax incentives for qualified energy projects are the primary reason high-earning professionals allocate capital to this sector. The economics are genuinely compelling, but the structure of each incentive type varies significantly.

The Section 48 ITC provides a credit equal to a percentage of the qualified investment in an eligible energy property. The base credit rate is 6%, rising to 30% when prevailing wage and apprenticeship requirements are met. Domestic content adders, energy community adders, and low-income community adders can push effective credit rates even higher, sometimes to 50% or more of qualified project costs.

The 48C credit allocations work differently. Projects apply competitively to the Department of Energy for a portion of the $10 billion pot, with DOE scoring based on technical merit and GHG reduction potential. Once allocated, the credit equals 30% of eligible property costs (or 6% without labor requirements).

State-level incentives add another layer. Key examples include:

- Ohio PILOTs: Solar projects certified as qualified energy projects are exempt from property taxes in exchange for payments in lieu of taxes (PILOTs) ranging from $7,000 to $9,000 per MW annually.

- County approval rules: Ohio projects exceeding 20 MW must obtain county board approval before tax abatement applies.

- Texas Energy Fund loans: The Texas Energy Fund provides 20-year loans at 3% interest, covering up to 60% of capital costs for qualifying electric facility construction and modernization.

The IRA expanded eligibility for tax-exempt entities such as nonprofits and Tribal governments through a “Direct Pay” mechanism, allowing them to receive the full ITC value as a cash reimbursement rather than a tax credit. This has broadened the investment ecosystem considerably, creating new co-investment structures between tax-equity investors and mission-driven organizations.

For investors with tax liability, transferability provisions now allow credits to be sold to third parties. This has turned tax credit monetization into a liquid market, with credits from qualified energy projects trading at 90 to 96 cents on the dollar in recent deal flow.

Explore how energy tax deduction strategies interact with these federal and state incentives to build a full picture of your after-tax return.

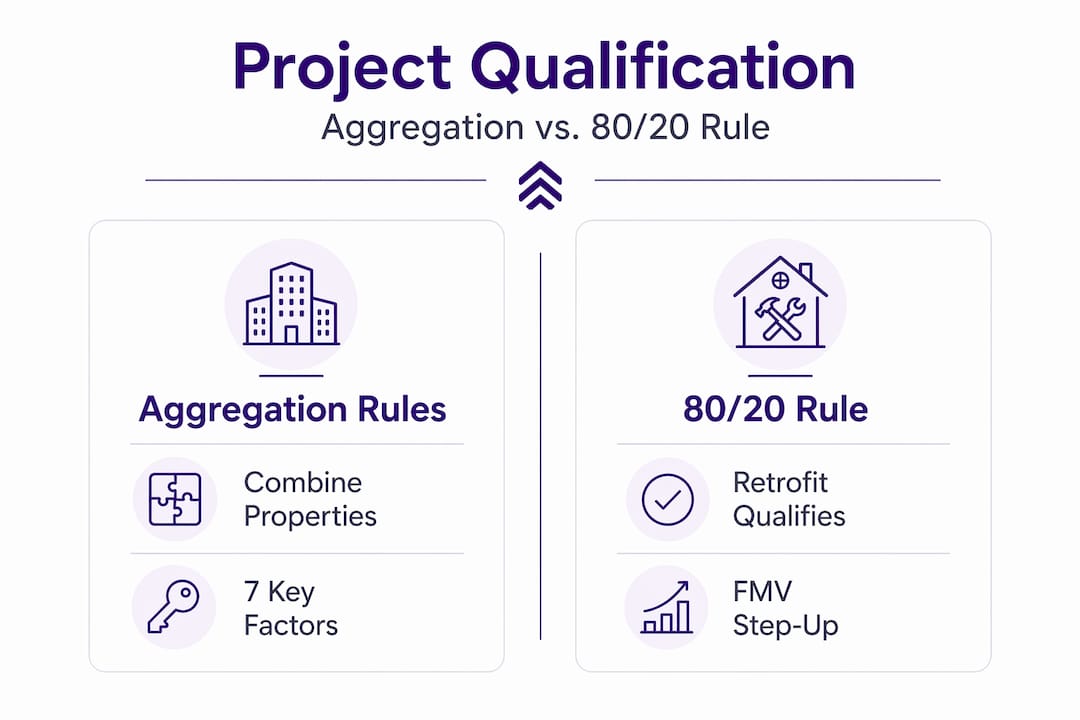

IRS aggregation rules and project qualification nuances

This is where most investors leave money on the table, or unknowingly create compliance exposure. The IRS does not treat every physical installation as a separate project by default.

Under final IRS regulations, multiple energy properties are treated as a single energy project when they share at least four of seven enumerated factors. Those factors include: land contiguity, a common power purchase agreement (PPA), connection to the same substation, shared permits, shared loan agreements, a single master construction contract, and construction by the same contractor.

Why does this matter? Because treating multiple facilities as a single project affects how capacity thresholds, adder eligibility, and credit base calculations are applied. In some cases, aggregation is beneficial. In others, it creates a larger “single project” that loses eligibility for certain capacity-based adders.

| Credit Program | Project Definition | Adder Assessment |

|---|---|---|

| Legacy Section 48 | Project-wide aggregation | Applies to the combined project |

| New Section 48E | Individual facility evaluation | Assessed per facility or storage tech |

The table above captures a critical point from legal experts: legacy and new credit programs use different “energy project” definitions, requiring separate eligibility analysis depending on when the project was placed in service.

Another overlooked provision is the 80/20 fair market value rule. A retrofitted or repowered facility can still qualify as originally placed in service for tax credit purposes, provided the value of used components does not exceed 20% of the total fair market value of the finished property. This opens significant opportunity for investors targeting brownfield repowering deals where new equipment is installed into an existing structure.

Pro Tip: Investors can also apply fair market value step-up strategies to increase the tax basis on qualified energy projects, thereby maximizing credit calculations while remaining within IRS compliance frameworks. This requires coordination with qualified tax counsel.

The election point also matters. Taxpayers elect whether to aggregate multiple properties either during construction or in the year of service. Locking in that election early can prevent later disputes with the IRS about project boundaries.

State programs and real-world examples

Federal rules provide the framework, but state programs often determine whether a specific qualified energy project pencils out financially. Two states illustrate the range well.

Ohio’s tax abatement program is one of the most structured state-level programs for solar. Projects certified as qualified energy projects receive full real and personal property tax exemptions. In return, they pay PILOTs of $7,000 to $9,000 per MW annually. For a 100 MW solar farm, that’s $700,000 to $900,000 per year in PILOT payments instead of full property tax liability, which for large installations could easily be several times higher. Projects above 20 MW go through a county approval process, which introduces a negotiation dynamic that sophisticated investors can use to their advantage when structuring deals.

Texas operates differently, using debt financing rather than tax exemptions. The Texas Energy Fund has backed projects totaling 3.47 GW in capacity as of May 2026, offering 20-year loans at 3% interest that cover up to 60% of capital costs. These loans are designed for electric facility construction and modernization. Infrastructure projects that improve grid reliability may also qualify under updated DOE Title 17 guidance, which now covers conventional infrastructure alongside innovative technologies.

The interaction between state and federal incentives is where experienced investors earn outsized returns. A Texas solar-plus-storage project, for example, could access Section 48E credits at the federal level, a Texas Energy Fund loan for capital cost coverage, and additional domestic content adders if equipment sourcing qualifies. Each layer compounds the effective return on invested capital. For a closer look at how state-specific incentives stack with federal programs, the evaluation framework applies directly to these multi-incentive structures.

My perspective: what most investors miss about qualified energy project eligibility

I’ve seen investors with real capital walk away from strong qualified energy project deals because the aggregation rules confused them. They assumed the IRS would treat a two-facility solar development as two separate projects, ran their credit math accordingly, and then panicked when legal review came back showing the facilities would be aggregated into one. That is not a reason to walk. It’s a reason to model both scenarios.

What I’ve learned is that aggregation rules are tools, not traps. When you understand the seven aggregation factors, you can structure deal terms to either consolidate or separate facilities depending on which outcome maximizes your credit position.

The other thing I’d push back on is the assumption that retrofits don’t qualify. The 80/20 rule changes that math entirely. Repowering an older wind facility with new turbines while keeping the existing substation and grid connection infrastructure is not a disqualifying factor. It’s a capital-efficient path to a fresh placed-in-service date. Investors who dismiss these deals on the surface are leaving real yield behind.

My honest take: the complexity of qualified energy project eligibility is not a problem. It’s a moat. Most investors won’t do the work to understand IRS aggregation rules, Section 48 versus 48E distinctions, and state-level PILOT structures. The ones who do are getting better deals with better tax profiles than the competition.

— Sharif

How Fieldvest helps you invest in qualified energy projects

Understanding qualified energy project eligibility is one thing. Accessing vetted deals that actually deliver on the tax and income potential is another. Fieldvest connects accredited investors with proven U.S. energy operators, focusing on projects that generate large first-year tax deductions alongside long-term cash flow. Whether you’re targeting oil and gas intangible drilling cost deductions or evaluating energy investments for your portfolio, Fieldvest provides the operator relationships and deal transparency you need. Use the free tax deduction calculator to estimate your first-year deduction, or run your numbers through the after-tax growth calculator to model long-term compound returns. Start with Fieldvest’s investment platform to see current opportunities.

FAQ

What is a qualified energy project under federal tax law?

A qualified energy project is any facility that generates electricity or heat using an eligible technology and meets the technical requirements for a specific federal tax credit such as the Section 48 ITC or Section 48C advanced energy credit. The exact definition varies by program.

What technologies qualify for energy project tax credits?

Solar, wind, geothermal, fuel cells, energy storage, offshore wind, and combined heat and power systems qualify under Section 48. Section 48E extends to any zero-emission technology, broadening eligibility beyond the legacy list.

How do IRS aggregation rules affect energy project qualification?

Multiple energy properties are treated as a single project when they share four or more of seven factors including land contiguity, shared permits, or a common PPA. This affects credit calculations, capacity thresholds, and adder eligibility.

Can a retrofit or repowered facility qualify as a new energy project?

Yes. The 80/20 rule allows a retrofitted facility to qualify as originally placed in service for tax credit purposes, as long as used components represent no more than 20% of the total fair market value.

What state programs support qualified energy projects?

Ohio offers property tax exemptions with PILOT payments of $7,000 to $9,000 per MW for certified solar projects. Texas provides 20-year loans at 3% interest through the Texas Energy Fund, covering up to 60% of capital costs for qualifying facilities.

Recommended

- Safe Energy Investing Platform: How to Evaluate Risk, Access, and Protection | Oil & Gas Investing

- What is upstream energy investing? A guide for accredited investors | Oil & Gas Investing

- Trusted Energy Investing Partner: How to Assess Clarity and Long-Term Value | Oil & Gas Investing

- Streamline Energy Investment Process: How Can It Really Be This Simple? | Oil & Gas Investing

Join our monthly energy

market Insights Newsletter